Protect Your Savings: Navigating 2026 Interest Rate Hikes and 3%+ Inflation

As we approach the mid-point of the decade, the economic landscape is showing signs of significant shifts that could profoundly impact personal finances. Specifically, the prospect of interest rate hikes in 2026, coupled with persistent inflation above 3%, presents a dual challenge for savers. For many, the instinct is to simply keep money in traditional savings accounts, but in an environment of rising costs and potentially higher borrowing expenses, this passive approach could lead to a significant erosion of purchasing power. Understanding these macroeconomic forces and adopting proactive strategies to protect savings inflation becomes not just advisable, but essential. This comprehensive guide will delve into the intricacies of these economic trends, analyze their potential impact, and, most importantly, equip you with actionable strategies to safeguard your financial future.

Understanding the Economic Landscape: 2026 Outlook

The year 2026 is shaping up to be a critical juncture for the global economy. While precise predictions are always challenging, several indicators suggest a period characterized by both rising interest rates and sustained inflation. Central banks worldwide have been grappling with inflationary pressures stemming from supply chain disruptions, increased consumer demand, and geopolitical tensions. To combat this, they often resort to increasing benchmark interest rates. This move, while necessary to cool down an overheating economy, has direct implications for everything from mortgage rates to the returns on your savings accounts.

Inflation, particularly if it remains above the Federal Reserve’s target of around 2%, means that the purchasing power of your money diminishes over time. If your savings are earning less than the rate of inflation, you are effectively losing money. For instance, if inflation is at 3% and your savings account yields 1%, your real return is a negative 2%. This is why strategies to protect savings inflation are paramount.

The interplay between interest rates and inflation is complex. Higher interest rates can sometimes curb inflation by making borrowing more expensive, thereby reducing demand. However, the lag effect of these policies means that inflation might persist for some time even after rates begin to climb. Therefore, anticipating these trends and positioning your finances accordingly is crucial for financial resilience in 2026 and beyond.

The Threat of Inflation Above 3%: Why It Matters for Your Savings

An inflation rate consistently above 3% is more than just a number; it’s a direct assault on your hard-earned savings. Imagine a basket of goods and services that costs $100 today. With 3% inflation, that same basket will cost $103 next year. If your money isn’t growing at least at that rate, you’re falling behind. This phenomenon, often referred to as the ‘silent tax,’ erodes wealth gradually but relentlessly.

The impact is felt across various aspects of daily life. The cost of groceries, utilities, housing, transportation, and healthcare all tend to rise. For retirees or those living on fixed incomes, this can be particularly devastating, as their income doesn’t adjust to the increased cost of living. Even for those with stable employment, the real value of their wages might decrease if pay raises don’t keep pace with inflation. Therefore, understanding how to actively protect savings inflation is not just for the wealthy; it’s a fundamental aspect of financial planning for everyone.

Moreover, sustained inflation can lead to uncertainty in financial markets, impacting investment valuations and making long-term financial planning more challenging. The goal isn’t just to make your money grow, but to ensure it grows faster than the rate at which its value is eroding. This requires a shift from passive saving to active wealth preservation and growth strategies.

Interest Rate Hikes in 2026: The Double-Edged Sword

While inflation erodes purchasing power, rising interest rates present a different set of challenges and opportunities. For borrowers, higher rates mean more expensive loans – mortgages, car loans, personal loans, and credit card debt all become costlier. This can stifle consumer spending and economic growth, which is often the central bank’s intention to cool inflation.

However, for savers, rising interest rates can be a silver lining, but only if they act strategically. Traditional savings accounts, certificates of deposit (CDs), and money market accounts might offer slightly better returns. Yet, it’s crucial to compare these returns against the inflation rate. If the interest earned is still less than inflation, your money is still losing value in real terms. The key is to seek out financial products and investment vehicles that offer returns competitive with or exceeding the inflation rate.

The challenge lies in timing and selection. Locking into long-term, low-yield investments just before rates rise can be disadvantageous. Conversely, being too conservative and missing out on opportunities for higher returns can also be detrimental. This balancing act is where informed decision-making and a clear strategy to protect savings inflation become indispensable.

Strategies to Protect Your Savings from Inflation and Rate Hikes

Navigating this complex economic environment requires a multi-faceted approach. Here are several strategies to consider for safeguarding your savings:

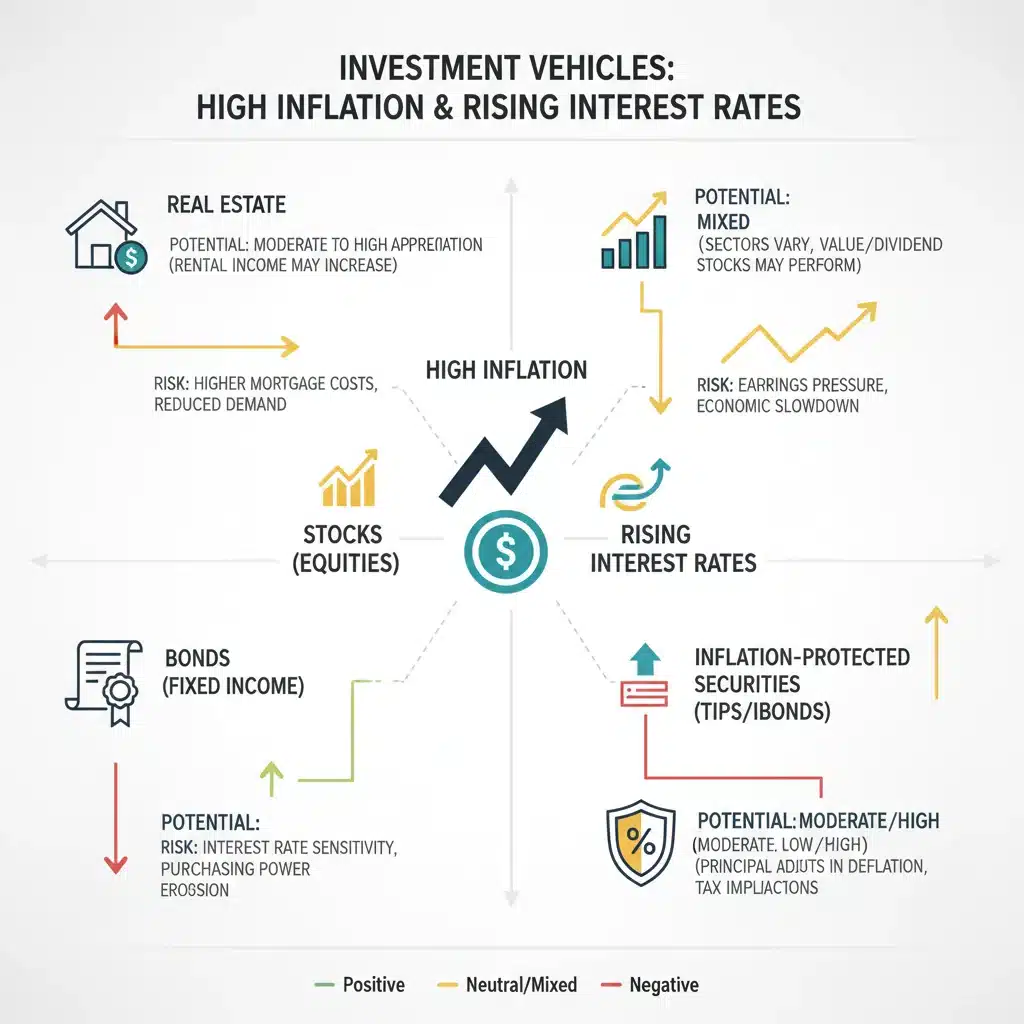

1. Invest in Inflation-Protected Securities (TIPS)

Treasury Inflation-Protected Securities (TIPS) are bonds issued by the U.S. Treasury that are indexed to inflation. The principal value of TIPS adjusts with the Consumer Price Index (CPI), so when inflation rises, the principal value of your TIPS also increases. This adjustment protects your investment’s purchasing power. While their yields might be lower than traditional bonds, the inflation protection they offer can be invaluable during periods of high inflation. They are a direct way to protect savings inflation.

2. Diversify Your Investment Portfolio

A well-diversified portfolio is your best defense against market volatility and economic shifts. Consider a mix of asset classes that tend to perform well under different economic conditions:

- Equities (Stocks): Historically, stocks have outperformed inflation over the long term. Companies that can pass on higher costs to consumers are particularly resilient. Focus on strong, established companies with pricing power.

- Real Estate: Real estate can be a good hedge against inflation as property values and rental income tend to rise with inflation. Consider direct property ownership, Real Estate Investment Trusts (REITs), or real estate funds.

- Commodities: Gold, silver, and other commodities often perform well during inflationary periods as they are tangible assets with intrinsic value.

Remember that diversification doesn’t eliminate risk, but it spreads it out, increasing the likelihood that at least some parts of your portfolio will perform well.

3. Re-evaluate Your Savings Accounts and CDs

With rising interest rates, it’s crucial to shop around for the best high-yield savings accounts and Certificates of Deposit (CDs). Don’t stick with your traditional bank if they offer meager returns. Online banks often provide more competitive rates. For CDs, consider a ‘CD laddering’ strategy: investing in CDs of varying maturities (e.g., 1-year, 2-year, 3-year). As shorter-term CDs mature, you can reinvest them at potentially higher prevailing interest rates, allowing you to benefit from rising rates while still having some liquidity.

4. Consider Floating-Rate Bonds and Loans

Unlike fixed-rate bonds, floating-rate bonds have interest payments that adjust periodically based on a benchmark interest rate. This means that as interest rates rise, the income you receive from these bonds will also increase, offering a degree of protection against rising rates. Similarly, if you are a lender or have investments in lending platforms, floating-rate loans can be advantageous.

5. Minimize High-Interest Debt

As interest rates rise, the cost of servicing variable-rate debt, such as credit card balances or adjustable-rate mortgages, will increase significantly. Prioritizing the payoff of these debts now can save you substantial amounts in interest payments down the line. If you have a fixed-rate mortgage at a low rate, it might be advisable to keep it, but aggressively tackle any high-interest, variable debt.

6. Invest in Your Skills and Earning Potential

One of the most effective long-term strategies to combat inflation and maintain your financial standing is to increase your earning power. Invest in education, acquire new skills, or seek certifications that make you more valuable in the job market. A higher income stream provides a stronger buffer against rising costs and allows you to save and invest more aggressively. This is an indirect but powerful way to protect savings inflation by increasing your capacity to generate wealth.

7. Review and Adjust Your Budget

Inflation makes everything more expensive, so a rigorous review of your budget is essential. Identify areas where you can cut back on discretionary spending. This might mean reducing subscriptions, eating out less, or finding more cost-effective alternatives for everyday purchases. Every dollar saved and invested strategically is a dollar protected from inflation.

8. Don’t Neglect Your Emergency Fund

While investing to beat inflation is crucial, maintaining a robust emergency fund is equally important. Ensure you have at least 3-6 months’ worth of living expenses readily accessible in a high-yield savings account. This fund provides a safety net for unexpected expenses, preventing you from having to dip into long-term investments or incur high-interest debt during challenging economic times.

9. Seek Professional Financial Advice

The economic landscape can be complex, and individual financial situations vary greatly. Consulting with a qualified financial advisor can provide personalized strategies tailored to your specific goals, risk tolerance, and current financial standing. An advisor can help you assess your portfolio, identify potential vulnerabilities, and recommend specific actions to protect savings inflation effectively.

Long-Term Perspective: Beyond 2026

While the focus here is on 2026, it’s important to remember that financial planning is an ongoing process. Economic cycles are a natural part of the market, and periods of inflation and rising interest rates will occur again. By developing a robust financial framework now, you’ll be better prepared for future economic shifts.

This involves consistent monitoring of economic indicators, regular reviews of your investment portfolio, and a willingness to adapt your strategies as circumstances change. The principles of diversification, debt management, and continuous learning remain timeless and are the bedrock of long-term financial security. Don’t let short-term anxieties overshadow your long-term vision. Instead, use the insights gained from anticipating 2026’s challenges to build a more resilient financial future.

Common Pitfalls to Avoid When Protecting Savings

While implementing strategies to protect savings inflation, it’s equally important to be aware of common mistakes that can undermine your efforts:

- Panic Selling: During periods of market volatility or economic uncertainty, some investors panic and sell off their investments, often locking in losses. A long-term perspective and a diversified portfolio can help mitigate the urge to make emotional decisions.

- Ignoring Inflation: The ‘silent tax’ of inflation is often underestimated. Failing to account for its corrosive effect on purchasing power is a critical error. Always consider real returns (returns after inflation) when evaluating investments.

- Putting All Eggs in One Basket: Concentrating all your investments in a single asset class or a few stocks can expose you to excessive risk. Diversification is key.

- Neglecting Debt: Allowing high-interest debt to accumulate, especially variable-rate debt, will severely counteract any gains you make from smart investments during a rising interest rate environment.

- Lack of Review: Financial plans are not set it and forget it. Regular review and adjustment are necessary to ensure your strategies remain aligned with current economic conditions and your personal goals.

By avoiding these pitfalls, you can enhance the effectiveness of your strategies and better secure your financial position.

The Role of Technology in Safeguarding Your Finances

In today’s digital age, technology offers numerous tools to help you manage and protect your finances. Financial planning apps can help you track your spending, create budgets, and monitor your investments. Robo-advisors can provide automated, diversified investment portfolios tailored to your risk tolerance, often at a lower cost than traditional financial advisors. Online banking platforms make it easier to compare interest rates, transfer funds, and manage multiple accounts.

Furthermore, staying informed through reputable financial news sources, podcasts, and online educational platforms can empower you to make more informed decisions. Leveraging these technological resources can significantly enhance your ability to proactively protect savings inflation and navigate the complexities of the 2026 economic outlook.

Conclusion: Proactive Steps for a Secure Financial Future

The anticipated economic shifts in 2026, marked by potential interest rate hikes and inflation above 3%, demand a proactive and informed approach to personal finance. Simply letting your money sit in traditional savings accounts is no longer a viable strategy for preserving wealth. Instead, a combination of strategic investments, debt management, budgeting, and continuous financial education will be crucial.

By understanding the mechanisms of inflation and interest rates, diversifying your portfolio, seeking out inflation-protected assets, and prudently managing debt, you can effectively protect savings inflation and ensure your financial well-being. The time to act is now. Start reviewing your financial situation, consulting with experts, and implementing these strategies to build a resilient financial future that can withstand the economic challenges ahead.

Remember, financial security is not about avoiding all risks, but about understanding them and positioning yourself to mitigate their negative impacts while capitalizing on opportunities. Take control of your financial destiny and navigate the coming years with confidence and foresight.