2026 Housing Market: Federal Interventions & 3% Price Growth Forecast

The landscape of the American dream, often encapsulated in homeownership, is perpetually evolving. As we cast our gaze forward to the

The past few years have been a rollercoaster for real estate, marked by historic low interest rates fueling bidding wars, followed by rapid rate hikes that cooled demand. Now, as the market seeks equilibrium, the

Understanding the nuances of this projection requires a comprehensive look at several key drivers. Inflation, though easing, remains a concern, influencing both construction costs and consumer purchasing power. Interest rates, while unlikely to return to their historic lows, are expected to stabilize, providing more predictability for mortgage borrowers. Supply and demand dynamics, always central to housing, continue to be critical, with ongoing inventory shortages in many desirable areas. Furthermore, demographic shifts, particularly the large millennial generation reaching prime homebuying age, will sustain underlying demand.

Central to the narrative of the

The Economic Backdrop: Inflation, Interest Rates, and Labor Market

The health of the broader economy is inextricably linked to the performance of the

By 2026, it is anticipated that inflation will have moderated further, settling closer to the Federal Reserve’s target rates. This stabilization is crucial. A predictable inflationary environment allows builders to plan more effectively and provides consumers with greater confidence in their long-term financial outlook. The Federal Reserve’s monetary policy, particularly its stance on interest rates, will continue to be a dominant force. While the era of near-zero interest rates is likely behind us, the expectation is for rates to stabilize at a level that is neither excessively restrictive nor overly stimulative. This ‘new normal’ for interest rates will allow the market to adjust and create a more sustainable borrowing environment.

The labor market’s strength also plays a vital role. A robust job market, characterized by low unemployment and steady wage growth, provides the income stability necessary for individuals and families to enter or remain in the housing market. Employment growth fuels demand, while wage increases help offset the impact of higher home prices and interest rates. The

Supply and Demand Dynamics: Bridging the Gap

One of the persistent challenges facing the housing market has been the chronic shortage of inventory. Years of underbuilding following the 2008 financial crisis, coupled with increased demand, created a significant supply-demand imbalance. This imbalance was a primary driver of rapid price appreciation during the pandemic. For the

Builders are gradually ramping up construction, driven by sustained demand and evolving market conditions. However, obstacles such as rising material costs, labor shortages, and stringent zoning regulations continue to impede the pace of new home construction. Federal and local governments are increasingly recognizing the urgency of this issue, exploring policies to streamline permitting processes, incentivize affordable housing development, and invest in infrastructure that supports new communities.

On the demand side, demographic trends are a powerful driver. The millennial generation, the largest adult generation, is increasingly entering their prime homebuying years. This demographic wave will continue to exert upward pressure on demand, particularly for entry-level and mid-range homes. Additionally, shifts in remote work continue to influence where people choose to live, potentially spreading demand to more affordable secondary markets, though primary metropolitan areas will likely retain their allure.

The 3% growth projection for the

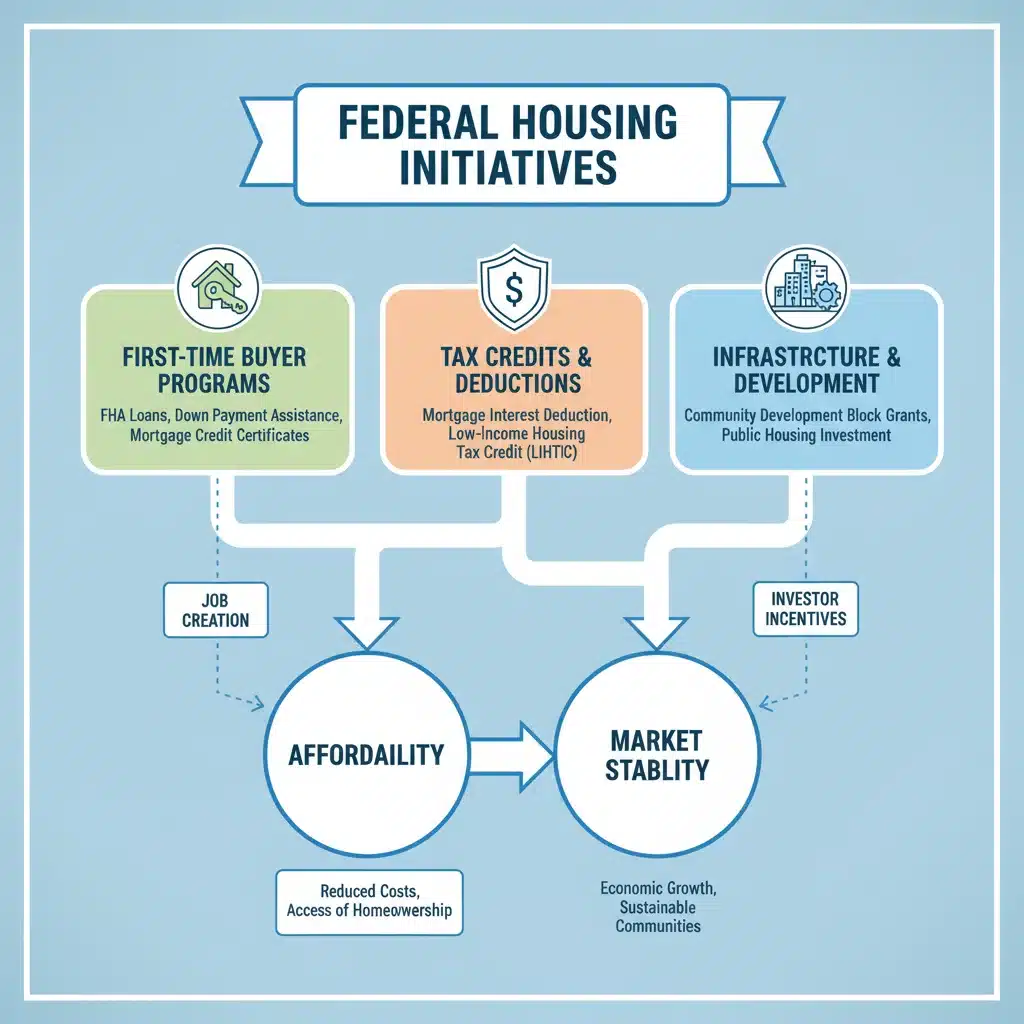

Federal Interventions: A Stabilizing Force

The federal government is not a passive observer in the housing market; its policies and programs exert considerable influence. For the

One critical area of intervention is through government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac. These entities play a crucial role in the secondary mortgage market, ensuring liquidity for lenders and setting standards for mortgage products. Their policies regarding loan limits, down payment assistance programs, and credit requirements directly impact who can qualify for a mortgage and under what terms. Anticipate continued efforts from these agencies to support first-time homebuyers and underserved communities.

The Federal Housing Administration (FHA) also provides vital support, particularly for buyers with lower down payments or less-than-perfect credit. FHA-insured loans are a cornerstone of affordable homeownership, and their continued availability and potential adjustments to their programs will be influential. The Department of Housing and Urban Development (HUD) oversees various initiatives aimed at increasing housing supply, combating homelessness, and enforcing fair housing laws.

Beyond these direct housing agencies, broader economic policies from the Treasury Department and the Federal Reserve have profound effects. Stable fiscal policy, responsible government spending, and predictable monetary policy all contribute to an economic environment conducive to a healthy housing market. The projected 3% growth in the

Mortgage Rates and Affordability: The Buyer’s Challenge

Mortgage rates are arguably the most significant factor influencing housing affordability for most buyers. The rapid ascent of rates in 2022 and 2023 significantly cooled demand by increasing monthly housing costs, even as home prices began to moderate. For the

This stabilization will provide more certainty for buyers, allowing them to better budget for homeownership. However, affordability will remain a key challenge. Even with a projected 3% price growth, home prices in many areas are still elevated relative to historical averages and income levels. This means that while the pace of appreciation slows, the absolute cost of housing remains a barrier for many.

Federal and state governments are likely to continue exploring and expanding programs designed to improve affordability. These include down payment assistance programs, first-time homebuyer tax credits, and initiatives to reduce closing costs. Furthermore, innovative financing solutions, such as shared equity programs or community land trusts, may gain more traction as alternatives to traditional homeownership models. The goal is to ensure that the

The interplay between wage growth and interest rates will be critical. If wage growth can keep pace with or exceed the rate of home price appreciation and interest rates remain stable, then affordability could gradually improve. Conversely, if wages stagnate while rates remain elevated, the affordability crunch will persist, potentially dampening demand despite other positive market indicators.

Regional Variations and Market Segmentation

It’s crucial to remember that the

Some areas, particularly those with strong job markets and continued in-migration, may see appreciation slightly above the national average. Conversely, regions facing economic headwinds, out-migration, or an abundance of new construction could experience flatter growth or even slight corrections. Coastal markets, often characterized by high demand and limited supply, may continue to see robust, albeit slower, appreciation. Inland markets and Sun Belt cities, which experienced significant booms, might see more moderate growth as they digest recent price gains.

Market segmentation also plays a role. The demand for single-family homes, particularly those in suburban areas with good schools and amenities, is likely to remain strong. The condominium and multi-family market, especially in urban cores, will be influenced by evolving work patterns and preferences for walkable communities. Luxury housing, often less sensitive to interest rate fluctuations, will follow its own dynamics, though it’s not immune to broader economic trends.

For both buyers and sellers in the

The Role of Technology and Innovation

Technology continues to transform the real estate industry, and its impact on the

Proptech (property technology) innovations are also influencing how homes are bought, sold, and managed. Online platforms make it easier for buyers to search for properties and connect with agents. Digital mortgage applications expedite the lending process. Smart home technologies are becoming standard features, influencing buyer preferences and potentially property values. The integration of artificial intelligence in market forecasting and personalized recommendations will further refine the home search and transaction process.

Furthermore, innovations in construction techniques, such as modular building and 3D printing, hold the potential to address the supply shortage by reducing construction times and costs. While these technologies may not fully revolutionize the market by 2026, their growing adoption will contribute to a more efficient and potentially more affordable housing supply in the long run. The

Investment Opportunities and Risks

For investors, the

Focus areas for investors might include markets with strong job growth, favorable demographic trends, and a clear path to increased housing supply. Rental properties in areas with high demand and low vacancy rates could continue to be appealing. Additionally, investing in properties that require renovation or value-add improvements could yield higher returns, assuming sound financial planning and execution.

Risks for investors include continued high interest rates impacting financing costs, potential oversupply in certain submarkets due to new construction, and regulatory changes that could affect landlord-tenant laws or property taxes. Geopolitical events and unforeseen economic shocks always pose risks to any market, and housing is no exception. Due diligence, market research, and a clear understanding of local economic conditions will be crucial for successful real estate investment in the

Preparing for the 2026 Housing Market: Advice for Buyers and Sellers

For prospective homebuyers, the

It’s also advisable to research local markets thoroughly. Understand the specific dynamics of the neighborhoods you’re interested in, including recent sales data, inventory levels, and future development plans. Be prepared to be flexible with your criteria and consider alternatives like townhouses or condos if single-family homes remain out of reach. Engaging with a knowledgeable local real estate agent will be indispensable for navigating these complexities.

Sellers in the

Understanding the current buyer pool and their preferences will also be important. Energy efficiency, smart home features, and dedicated home office spaces continue to be highly valued. Sellers should be prepared for potential negotiations and allow for reasonable inspection contingencies. Working with an experienced real estate professional who understands local market trends and can effectively market your property will be key to a successful sale in the

Conclusion: A Path Towards Stable Growth

The

While challenges such as ongoing affordability concerns and regional disparities will persist, the overall outlook suggests a more predictable and less volatile environment for both buyers and sellers. The evolving role of technology and continued demographic shifts will further shape the market, creating new opportunities and demanding adaptive strategies from all participants. By understanding these intricate dynamics and preparing accordingly, individuals and investors can navigate the