Credit Score Optimization 2026: Boost Your FICO 50+ Points in 6 Months

Credit Score Optimization 2026: Boost Your FICO 50+ Points in 6 Months

In today’s dynamic financial landscape, a strong credit score is more than just a number; it’s a powerful tool that unlocks opportunities, saves you money, and provides peace of mind. As we navigate through 2026, understanding the nuances of FICO score optimization has become increasingly critical. Whether you’re looking to secure a new home loan, get better rates on auto financing, or simply enhance your financial standing, boosting your FICO score by 50+ points in just six months is an achievable goal with the right strategies and consistent effort. This comprehensive guide will walk you through the essential steps, expert tips, and common pitfalls to avoid, ensuring your FICO score optimization journey is successful and sustainable.

Many individuals find themselves in a challenging situation where their credit score is not where they’d like to be. This can be due to a variety of factors, from past financial missteps to simply not knowing how the credit system works. The good news is that credit scores are not static; they are dynamic and can be improved with targeted actions. Our focus here is on FICO score optimization, as FICO scores are the most widely used by lenders, impacting everything from mortgage approvals to insurance premiums. By understanding the key components that make up your FICO score and implementing strategic changes, you can significantly improve your financial health in a relatively short period.

The journey to a higher FICO score begins with a clear understanding of your current credit situation. This involves regularly checking your credit reports from all three major bureaus—Experian, Equifax, and TransUnion—and identifying any inaccuracies or areas that need improvement. Disputing errors, managing debt effectively, and making timely payments are foundational elements of any successful FICO score optimization plan. We’ll delve into each of these areas, providing actionable advice that you can start implementing today to see tangible results within the next six months. Prepare to take control of your financial future and unlock the benefits of an optimized FICO score.

Understanding Your FICO Score: The Foundation of Optimization

Before embarking on any FICO score optimization efforts, it’s crucial to grasp what a FICO score is and how it’s calculated. FICO, or Fair Isaac Corporation, is the most common credit scoring model used by lenders. Your FICO score is a three-digit number, typically ranging from 300 to 850, that represents your creditworthiness. A higher score indicates a lower risk to lenders, making you eligible for better interest rates and more favorable terms on loans and credit products.

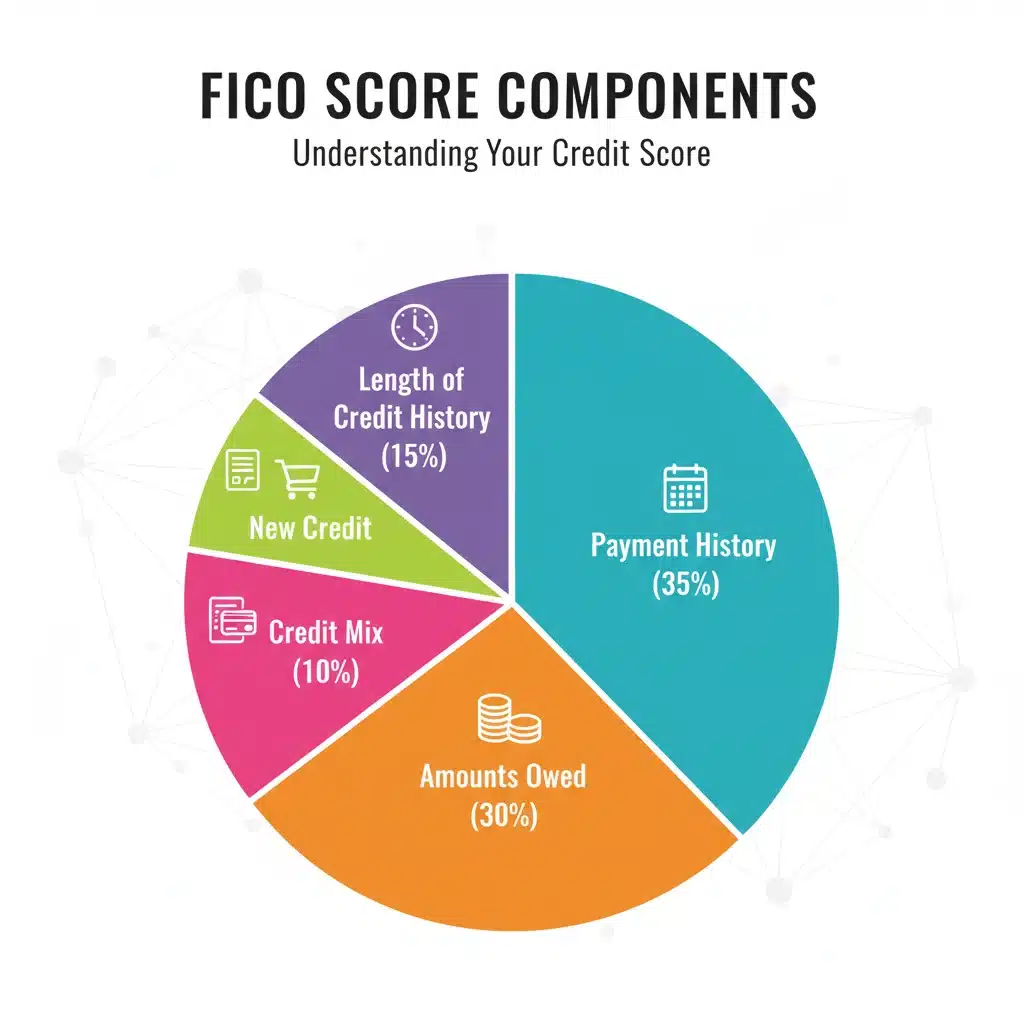

The FICO scoring model considers five main categories, each weighted differently:

- Payment History (35%): This is the most significant factor. Paying your bills on time, every time, is paramount. Late payments, bankruptcies, collections, and charge-offs can severely damage your score.

- Amounts Owed (30%): This refers to your credit utilization, which is the amount of credit you’re using compared to your total available credit. Keeping your credit utilization low (ideally below 30%) is vital for FICO score optimization.

- Length of Credit History (15%): The longer your credit accounts have been open and in good standing, the better. This factor considers the age of your oldest account, the age of your newest account, and the average age of all your accounts.

- New Credit (10%): Opening too many new credit accounts in a short period can be seen as risky by lenders. This category also considers hard inquiries, which occur when you apply for new credit.

- Credit Mix (10%): Having a healthy mix of different types of credit accounts, such as revolving credit (credit cards) and installment loans (mortgages, auto loans), can positively impact your score.

Understanding these percentages is the first step towards effective FICO score optimization. By knowing which factors carry the most weight, you can prioritize your efforts and focus on areas that will yield the greatest impact on your score. For instance, if you consistently make late payments, addressing this issue will have a much larger effect than, say, slightly adjusting your credit mix. Regular monitoring of your credit report is essential to track progress and identify any discrepancies that might be holding your score back.

Phase 1: The First Month – Laying the Groundwork for FICO Score Optimization

The initial month of your FICO score optimization journey is all about assessment and foundational adjustments. Think of it as preparing the soil before planting the seeds for growth. This phase focuses on understanding your current credit health and addressing immediate issues.

1. Obtain and Review Your Credit Reports

Your first and most critical step is to get copies of your credit reports from all three major credit bureaus: Experian, Equifax, and TransUnion. You are entitled to one free report from each bureau annually through AnnualCreditReport.com. Carefully review each report for accuracy. Look for:

- Incorrect Personal Information: Names, addresses, employers, etc.

- Accounts You Don’t Recognize: This could indicate identity theft.

- Incorrect Payment Status: Make sure all payments are reported accurately as on-time.

- Duplicate Accounts: Sometimes an account might be listed twice.

- Outdated Information: Negative items should fall off your report after 7 years (10 for bankruptcy).

2. Dispute Any Errors Immediately

If you find errors, dispute them with the credit bureau and the information provider (e.g., the bank or creditor) as soon as possible. Each bureau has a specific process for disputes, usually involving submitting documentation online or by mail. Correcting inaccuracies can sometimes lead to an immediate jump in your FICO score. This is a vital part of FICO score optimization, as even a small error can negatively impact your score.

3. Create a Budget and Payment Plan

To ensure timely payments and effective debt reduction, creating a realistic budget is essential. Understand your income and expenses to identify areas where you can cut back and allocate more funds towards debt. Prioritize payments for accounts that are past due or nearing delinquency. Set up automatic payments whenever possible to avoid missing due dates, a cornerstone of improving your payment history.

4. Address Delinquent Accounts

If you have any accounts that are 30, 60, or 90+ days past due, immediately work to bring them current. Even one late payment can significantly drop your FICO score. If you’re struggling, contact your creditors to discuss potential payment plans or hardship programs. Getting current on delinquent accounts is a powerful first step in FICO score optimization.

Phase 2: Months 2-3 – Strategic Debt Management and Credit Utilization

With your foundation laid, the next two months focus on actively managing your debt and optimizing your credit utilization, which accounts for 30% of your FICO score. This is where you’ll start to see more significant movement in your score.

1. Reduce Your Credit Utilization Ratio

This is arguably the most impactful strategy for quick FICO score optimization. Your credit utilization ratio is the total amount of credit you’re using divided by your total available credit. Aim to keep this ratio below 30%, and ideally even lower, around 10% for the best results. For example, if you have a credit card with a $1,000 limit, try to keep your balance below $300.

- Pay Down Balances: Focus on paying down high-balance credit cards first.

- Make Multiple Payments: Instead of waiting for the statement due date, make smaller payments throughout the month to keep your reported balance low.

- Request Credit Limit Increases: If you have a good payment history with a particular card, requesting a credit limit increase (without increasing your spending) can lower your utilization. Be cautious, as this might trigger a hard inquiry.

2. Prioritize High-Interest Debt with the Debt Avalanche or Snowball Method

While paying down debt, choose a strategy: the debt avalanche method (paying off highest interest rate first) saves you money, while the debt snowball method (paying off smallest balance first) provides psychological wins. Both are effective for FICO score optimization as they reduce your overall debt burden.

3. Avoid Opening New Credit Accounts

During this critical period of FICO score optimization, resist the urge to open new credit cards or take out new loans. Each new application results in a hard inquiry, which can temporarily ding your score. New accounts also lower the average age of your accounts, negatively impacting your length of credit history.

4. Maintain On-Time Payments Consistently

Reinforce your new payment habits. Every on-time payment reported to the credit bureaus contributes positively to your payment history, the largest factor in your FICO score. Consistency is key here. If you missed payments in the past, a steady stream of on-time payments will gradually diminish their impact.

Phase 3: Months 4-6 – Fine-Tuning and Long-Term Strategies for FICO Score Optimization

In the final three months, you’ll be fine-tuning your credit profile and implementing strategies for sustained FICO score optimization. By now, you should be seeing noticeable improvements.

1. Become an Authorized User (Carefully)

If a trusted friend or family member with an excellent credit history and low credit utilization is willing, becoming an authorized user on one of their credit cards can be beneficial. Their positive payment history and low utilization can reflect on your report. However, ensure they maintain good credit habits, as their missteps could also affect you. This is a strategy that can accelerate FICO score optimization but requires careful consideration.

2. Consider a Secured Credit Card or Credit Builder Loan

If you have a limited credit history or a history of past issues, a secured credit card or a credit builder loan can be excellent tools. A secured credit card requires a deposit, which acts as your credit limit. A credit builder loan places the loan amount in a savings account that you access once payments are complete. Both help establish positive payment history and demonstrate responsible credit behavior without significant risk to the lender, contributing to FICO score optimization.

3. Diversify Your Credit Mix (If Appropriate)

Once your primary credit issues are resolved and your score has improved, strategically adding a different type of credit can be beneficial. For example, if you only have credit cards, consider a small installment loan. This should only be done if you genuinely need the credit and can comfortably manage the payments, as opening unnecessary accounts can be detrimental. Remember, this is a smaller factor (10%) in FICO score optimization.

4. Continue Monitoring Your Credit Reports

Even after significant FICO score optimization, ongoing monitoring is crucial. Check your reports regularly for any new errors or suspicious activity. This vigilance helps maintain your improved score and protects you from identity theft.

Common Pitfalls to Avoid During FICO Score Optimization

While striving for a higher FICO score, it’s easy to fall into common traps that can hinder your progress. Being aware of these pitfalls can save you time and prevent setbacks in your FICO score optimization journey.

1. Closing Old Credit Accounts

It might seem counterintuitive, but closing old credit cards, especially those with a zero balance, can actually hurt your FICO score. This is because closing an account reduces your total available credit, which can increase your credit utilization ratio. It also shortens your average length of credit history, another key FICO factor. Unless there’s an annual fee you can’t justify, or the temptation to overspend is too great, it’s often better to keep old accounts open, even if you don’t use them frequently.

2. Applying for Too Much New Credit

As mentioned earlier, each time you apply for new credit, a hard inquiry is placed on your report. While one or two inquiries might not severely impact your score, a flurry of applications in a short period can signal to lenders that you’re a higher risk, potentially indicating financial distress. This can lead to a temporary dip in your score and make future credit approvals more challenging. Be strategic and apply for credit only when truly necessary.

3. Ignoring Small Debts or Collections

Even a small unpaid balance can negatively impact your FICO score, especially if it goes to collections. While older collection accounts have less impact than newer ones, they remain on your report for up to seven years. Make an effort to pay off all outstanding debts, no matter how small, or negotiate a pay-for-delete arrangement if possible (though creditors are not obligated to agree). Addressing these lingering issues is crucial for comprehensive FICO score optimization.

4. Relying on ‘Quick Fix’ Credit Repair Services

Be wary of companies promising to drastically improve your credit score overnight or remove legitimate negative items from your report. Many of these services are scams or engage in unethical practices. True FICO score optimization takes time and consistent effort. Focus on legitimate strategies and direct communication with creditors and credit bureaus. If you need professional help, seek out non-profit credit counseling agencies.

5. Not Reviewing Your Credit Reports Regularly

Failure to regularly check your credit reports can lead to missed errors, potential identity theft, or simply a lack of awareness about your credit standing. Make it a habit to review your reports at least once a year, and consider using credit monitoring services that alert you to changes. Proactive monitoring is a cornerstone of maintaining and further enhancing your FICO score optimization efforts.

Advanced Strategies and Long-Term FICO Score Optimization

Once you’ve achieved your initial goal of boosting your FICO score by 50+ points, the journey doesn’t end there. Sustained financial health requires ongoing effort and the implementation of advanced strategies for long-term FICO score optimization.

1. Maintain Low Credit Utilization

This cannot be stressed enough. Consistently keeping your credit utilization below 10% on all your revolving accounts is ideal. The lower, the better. This demonstrates excellent credit management and signals to lenders that you’re not over-reliant on credit. Even if you pay your balance in full each month, consider paying it down before the statement closing date to ensure a low balance is reported to the credit bureaus.

2. Become a Master of On-Time Payments

Your payment history is 35% of your FICO score. A perfect payment history over several years is incredibly powerful. Continue to set up automatic payments, calendar reminders, or use budgeting apps to ensure you never miss a due date. This consistency is the backbone of long-term FICO score optimization.

3. Strategically Manage New Credit Applications

While avoiding new credit is good during initial repair, once your score is strong, you can strategically apply for new credit to diversify your credit mix or take advantage of better terms. However, always ensure you have a legitimate need for the credit and can comfortably manage the payments, as opening unnecessary accounts can be detrimental. Avoid opening new accounts just for the sake of it, as too many hard inquiries can still cause temporary dips.

4. Consider Experian Boost and UltraFICO

These relatively newer options can help some individuals with limited credit history or those looking for a slight edge. Experian Boost allows you to add positive payment history from utility bills and phone bills to your Experian report. UltraFICO uses your banking data (like checking and savings account activity) to provide an alternative FICO score, potentially beneficial if you manage your bank accounts well but have a thin credit file. These can be valuable tools for certain FICO score optimization scenarios.

5. Review Your Credit Account Limits Annually

Periodically, review your credit card limits. If you’ve been a responsible cardholder, some issuers may offer automatic credit limit increases. Alternatively, you can request an increase. As long as you don’t increase your spending, a higher credit limit will automatically lower your credit utilization ratio, contributing positively to FICO score optimization without new inquiries.

6. Understand the Impact of Public Records

Bankruptcies, foreclosures, and tax liens are public records that can severely damage your credit score and remain on your report for several years (7-10 years depending on the type). While these are difficult to remove if legitimate, understanding their impact and focusing on positive credit behaviors in the interim is crucial for recovery. As time passes and new positive information is added, their impact will gradually diminish.

The Benefits of a High FICO Score in 2026

Achieving significant FICO score optimization opens doors to a multitude of financial advantages in 2026. A higher score translates directly into more favorable financial terms, saving you substantial amounts of money over your lifetime.

1. Lower Interest Rates on Loans

This is perhaps the most significant benefit. Whether it’s a mortgage, an auto loan, or a personal loan, a higher FICO score qualifies you for the lowest available interest rates. Even a small percentage point difference can save you thousands or tens of thousands of dollars over the life of a loan. For example, on a $300,000 mortgage, a difference of just 0.5% in interest can mean saving over $10,000 in interest payments over 30 years. This alone makes FICO score optimization a worthwhile endeavor.

2. Easier Loan and Credit Card Approvals

Lenders view individuals with high FICO scores as less risky. This means you’re more likely to be approved for the credit products you apply for, including premium credit cards with attractive rewards programs and higher credit limits. This provides greater financial flexibility and access to funds when you need them.

3. Better Insurance Rates

In many states, insurance companies use credit-based insurance scores (which are derived from your credit report) to determine premiums for auto and home insurance. A higher FICO score often leads to lower insurance premiums, adding another layer of savings to your budget. This is an often-overlooked benefit of FICO score optimization.

4. Easier Apartment Rentals and Utilities Setup

Landlords frequently check credit scores as part of their tenant screening process. A strong FICO score can make it easier to secure an apartment, sometimes even waiving the need for a larger security deposit. Similarly, utility companies may waive deposits for new services if you have a robust credit history.

5. Enhanced Financial Flexibility and Peace of Mind

With a high FICO score, you have more control over your financial life. You’re better prepared for unexpected expenses, can take advantage of financial opportunities, and experience less stress about your financial standing. This peace of mind is invaluable and a direct result of effective FICO score optimization.

Conclusion: Your Path to FICO Score Optimization in 2026

Boosting your FICO score by 50+ points in six months is an ambitious yet entirely achievable goal for 2026. It requires dedication, consistency, and a strategic approach, but the financial rewards are well worth the effort. By understanding the components of your FICO score, diligently reviewing your credit reports, and implementing the strategies outlined in this guide—from consistent on-time payments and reducing credit utilization to strategic debt management and avoiding common pitfalls—you can significantly improve your credit health.

Remember, FICO score optimization is not a one-time event but an ongoing process. The habits you build over these six months will serve as the foundation for a lifetime of excellent financial standing. Regularly monitor your credit, stay disciplined with your payments, and continue to educate yourself on best financial practices. A strong FICO score is a powerful asset that will unlock better rates, greater opportunities, and profound financial peace of mind. Start your journey today and take control of your financial future!