Navigate 2026 Social Security Changes: What the 3.2% COLA Means for Your Annual Benefits

Navigating the Future: What the 3.2% Social Security COLA Means for Your 2026 Benefits

As we look ahead, understanding the nuances of your future financial landscape becomes increasingly vital. For millions of Americans, Social Security benefits form the bedrock of their retirement income. A significant factor influencing these benefits is the Cost-of-Living Adjustment, or COLA. For 2026, the projected Social Security COLA 2026 is an estimated 3.2%. While this might seem like just another number, its implications for your annual benefits and overall financial well-being are profound. This comprehensive guide will delve deep into what this projected COLA means, how it’s calculated, its historical context, and most importantly, how you can strategically plan to maximize your Social Security benefits in light of these changes.

The Social Security Administration (SSA) makes annual adjustments to benefits to ensure that the purchasing power of retirees and other beneficiaries is not eroded by inflation. This adjustment, the COLA, is a critical component of the system, designed to help beneficiaries keep pace with rising costs. A 3.2% Social Security COLA 2026 would represent a notable increase, impacting everything from monthly checks to annual financial planning. It’s not merely an increase; it’s a reflection of economic forces and a crucial element in maintaining financial stability for millions.

Understanding the intricacies of the Social Security COLA 2026 is more than just knowing a percentage; it’s about comprehending the economic indicators that drive it, the impact it has on your personal finances, and the proactive steps you can take to adapt. This article aims to equip you with the knowledge needed to navigate these changes effectively, ensuring you are well-prepared for the financial realities of 2026 and beyond.

Understanding the Social Security COLA: The Basics

The Cost-of-Living Adjustment (COLA) is an annual increase in Social Security and Supplemental Security Income (SSI) benefits. Its primary purpose is to counteract the effects of inflation, allowing beneficiaries to maintain their purchasing power as the cost of living rises. Without COLA, the value of Social Security benefits would steadily decline over time, making it increasingly difficult for retirees and other eligible individuals to afford essential goods and services.

The calculation of the COLA is tied directly to the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). Specifically, the SSA compares the average CPI-W for the third quarter (July, August, and September) of the current year with the average for the same period in the previous year. The percentage increase between these two periods determines the COLA. If there is no increase, there is no COLA. This methodology ensures that the adjustment reflects real-world price changes experienced by a significant portion of the population.

For the Social Security COLA 2026, the projected 3.2% is an estimate based on current economic forecasts and inflationary trends. It’s important to remember that this is a projection, and the final COLA will be announced by the SSA in October of the preceding year (in this case, October 2025). However, such projections often provide a reliable indication of what to expect, allowing for preliminary financial planning. A 3.2% increase, while not as high as some recent years, still represents a significant boost to annual benefits, especially when compounded over time.

The COLA affects all Social Security beneficiaries, including retirees, survivors, and individuals receiving disability benefits. It also applies to SSI benefits. This widespread impact underscores the importance of staying informed about these adjustments, as they directly influence the financial security of a vast segment of the American population.

The Projected 3.2% Social Security COLA 2026: What It Means for You

A 3.2% Social Security COLA 2026 signifies a tangible increase in your monthly and annual Social Security benefits. Let’s break down what this percentage increase could translate to in real terms. For example, if your current monthly Social Security benefit is $1,800 (which is close to the average for retired workers), a 3.2% COLA would add approximately $57.60 to your monthly check, bringing your new benefit to $1,857.60. Over a year, this amounts to an additional $691.20 in income. While this might not seem like a monumental sum for some, for many, especially those on fixed incomes, every dollar counts and contributes significantly to covering rising living expenses.

This increase is designed to help offset the impact of inflation. When the cost of goods and services rises, your money buys less. The COLA aims to restore some of that lost purchasing power. Therefore, the 3.2% Social Security COLA 2026 is not about making you wealthier in real terms but about maintaining your current standard of living in the face of ongoing economic changes.

The impact of this COLA extends beyond just the monthly check. It also affects the maximum amount of earnings subject to Social Security taxes, known as the Social Security wage base. This typically increases each year, reflecting wage growth and economic conditions. While the COLA directly impacts benefits, the wage base adjustment is relevant for current workers and their future benefit calculations. Furthermore, the COLA can indirectly influence other aspects of your financial planning, such as budgeting for healthcare costs, which often rise independently of COLA adjustments, but whose impact can be mitigated by an increased Social Security income.

Inflation and the COLA: A Symbiotic Relationship

The relationship between inflation and the Social Security COLA 2026 is fundamental. Inflation, simply put, is the rate at which the general level of prices for goods and services is rising, and consequently, the purchasing power of currency is falling. The COLA is a direct response to this economic phenomenon. When inflation is high, as it has been in recent years, the COLA tends to be higher to provide a more substantial boost to benefits. Conversely, during periods of low inflation, the COLA will be smaller, or in rare cases, non-existent.

The CPI-W, the index used to calculate the COLA, specifically tracks the prices of a basket of goods and services consumed by urban wage earners and clerical workers. This basket includes items like food, housing, transportation, medical care, and other everyday necessities. By comparing the CPI-W from one period to the next, the SSA can gauge the rate of inflation and adjust benefits accordingly. The projected 3.2% Social Security COLA 2026 suggests that while inflation might be moderating compared to previous peaks, it is still a significant factor impacting the economy and household budgets.

It’s crucial to understand that the CPI-W may not perfectly reflect the spending patterns of all Social Security beneficiaries, particularly seniors who often have different expenditure profiles (e.g., higher healthcare costs). This discrepancy can sometimes lead to discussions about whether the COLA adequately covers the actual cost of living for retirees. However, the CPI-W remains the statutory measure for COLA calculations. Therefore, staying informed about broader economic trends, especially inflation, provides valuable context for understanding the projected Social Security COLA 2026 and its real-world impact on your finances.

Historical COLA Trends and Future Projections

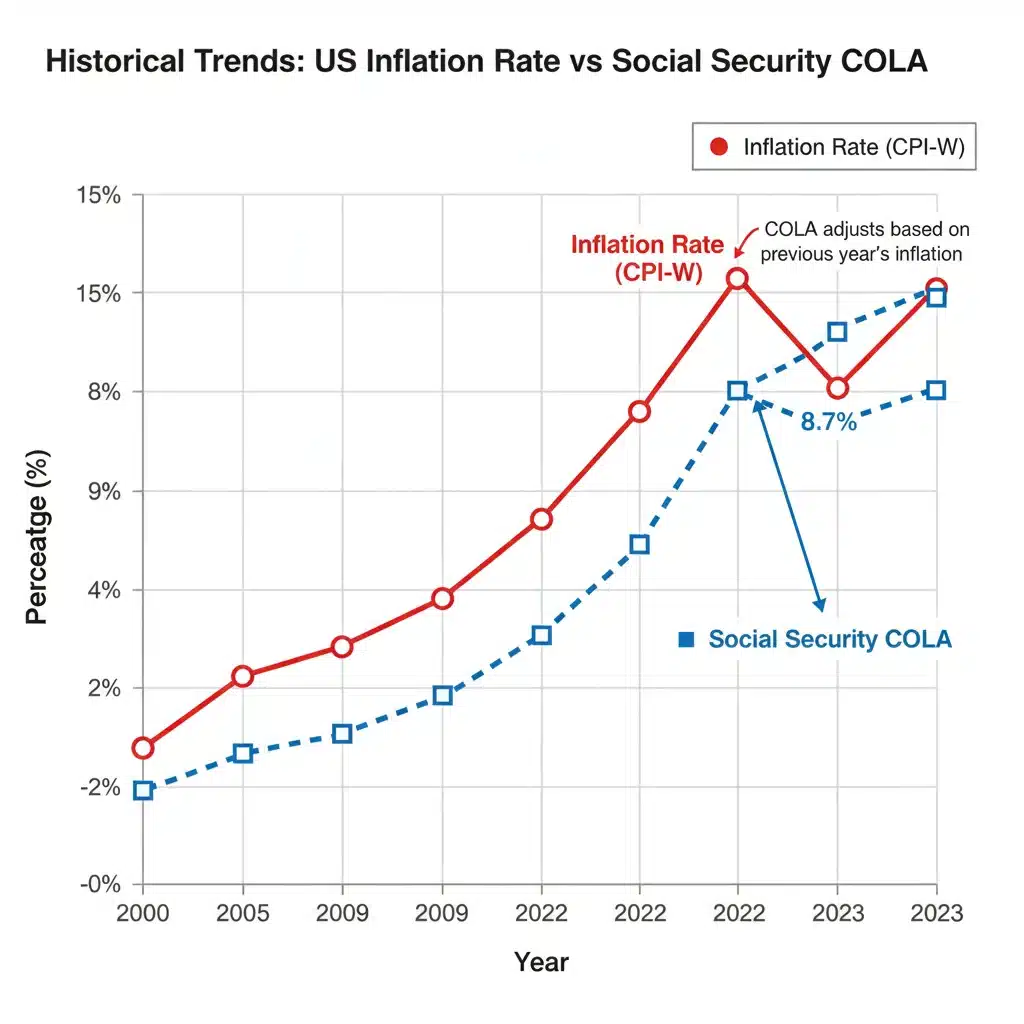

Looking at historical COLA trends provides valuable insight into what the 3.2% Social Security COLA 2026 might signify. In recent decades, COLA percentages have varied widely, reflecting different economic environments. For instance, the 2022 COLA was a substantial 5.9%, followed by an even larger 8.7% for 2023, driven by a surge in inflation. In contrast, there were years with zero COLA, such as 2010, 2011, and 2016, during periods of very low or negative inflation.

The projected 3.2% Social Security COLA 2026 falls somewhere in the middle of these extremes, suggesting a period of more moderate, yet still present, inflationary pressures. This projection is based on a variety of economic indicators, including forecasts for energy prices, food costs, and other consumer goods. Economic analysts and the Social Security Administration’s own actuaries continuously monitor these factors to provide the most accurate estimates possible.

Future projections for COLA are inherently uncertain, as they depend on unpredictable economic factors. However, the ongoing commitment to adjusting benefits for inflation remains a cornerstone of the Social Security program. While the exact percentage for future years cannot be known, understanding the mechanism and the current economic climate allows beneficiaries to anticipate and plan for these adjustments. The 3.2% Social Security COLA 2026, therefore, serves as a benchmark for what beneficiaries can expect, enabling them to make informed decisions about their retirement income and spending.

Eligibility for Social Security COLA 2026

Eligibility for the Social Security COLA 2026 is straightforward for most beneficiaries. If you are currently receiving Social Security benefits—whether as a retired worker, a spouse, a survivor, or due to disability—you will automatically receive the COLA. There is no special application process required. The adjustment is applied across the board to all eligible individuals, ensuring that everyone’s benefits keep pace with the cost of living.

For those who are not yet receiving benefits but plan to claim Social Security in 2026 or later, the COLA also plays a role. The adjustments apply to your benefit calculation even before you claim. For example, if you turn 62 in 2025 but delay claiming until 2026 or later, the COLA that applies to current beneficiaries in 2026 would effectively increase the value of your future benefits. This is because your primary insurance amount (PIA), the benefit you would receive at full retirement age, is adjusted for COLA in the years between when you turn 62 and when you claim benefits, up to the year you turn 62. This ensures that delaying your claim can potentially result in higher benefits, not just due to delayed retirement credits, but also due to COLA increases.

It’s important to note that while the COLA increases your gross benefit amount, certain factors can affect your net benefit. These include Medicare Part B premiums, which are often deducted directly from Social Security checks. While a COLA increases your benefits, a rise in Medicare premiums could potentially offset some of that gain. Therefore, when considering the impact of the Social Security COLA 2026, it’s essential to look at the full picture of your income and expenses.

Impact on Medicare Premiums and Taxes

One of the most critical considerations when assessing the impact of the Social Security COLA 2026 is its interaction with Medicare Part B premiums. By law, Medicare Part B premiums are often deducted directly from Social Security benefits. While the COLA increases your Social Security payment, a rise in Medicare premiums can sometimes consume a significant portion, or even all, of that increase. This phenomenon is often referred to as the "hold harmless" provision, which prevents Part B premiums from rising so much that a beneficiary’s net Social Security payment decreases from one year to the next. However, this provision doesn’t apply to everyone, and even when it does, it can limit the effective benefit of the COLA.

For those not covered by the "hold harmless" provision (e.g., new Medicare enrollees, those paying higher income-related monthly adjustment amounts (IRMAA), or those whose Part B premiums are paid by a state Medicaid program), increases in Part B premiums can directly reduce the net benefit from the COLA. Therefore, when the 3.2% Social Security COLA 2026 is announced, it’s equally important to pay attention to any projected changes in Medicare Part B premiums for the same year.

Furthermore, Social Security benefits can be subject to federal income tax for some individuals. If your "combined income" (adjusted gross income + nontaxable interest + half of your Social Security benefits) exceeds certain thresholds, a portion of your Social Security benefits may be taxable. A COLA increase, such as the projected 3.2% Social Security COLA 2026, could potentially push some beneficiaries into a higher tax bracket or increase the taxable portion of their benefits, even if their real purchasing power remains similar. This is an important consideration for financial planning and tax preparation, as it can subtly reduce the effective gain from the COLA.

Strategies to Maximize Your Social Security Benefits

Understanding the Social Security COLA 2026 is just one piece of the puzzle; proactively planning your Social Security strategy is vital to maximizing your benefits. Here are several key strategies to consider:

1. Delaying Claims Past Full Retirement Age (FRA): For every year you delay claiming Social Security benefits past your Full Retirement Age (up to age 70), you earn delayed retirement credits. These credits permanently increase your annual benefit by a certain percentage (typically 8% per year). Coupled with COLA increases, delaying can significantly boost your lifetime benefits. The 3.2% Social Security COLA 2026 will apply to your higher benefit amount if you delay, making the increase even more substantial.

2. Coordinating with a Spouse: If you are married, strategic coordination of when you and your spouse claim benefits can lead to higher combined lifetime benefits. This often involves the higher earner delaying their claim while the lower earner claims earlier, or one spouse claiming spousal benefits while deferring their own worker benefit. Understanding the various claiming strategies is crucial for maximizing family benefits.

3. Working Longer: Your Social Security benefit is based on your highest 35 years of earnings. If you have fewer than 35 years of earnings, or if your current earnings are higher than some of your earlier years, working longer can replace lower-earning years with higher-earning ones, thereby increasing your average indexed monthly earnings (AIME) and ultimately your benefit amount. Any COLA, including the Social Security COLA 2026, will then apply to this higher base.

4. Understanding Your Earnings Record: Regularly check your Social Security earnings record through your online "My Social Security" account. Ensure that all your earnings are accurately reported. Errors can lead to lower benefits, so correcting them promptly is essential.

5. Factoring in Inflation and COLA in Retirement Planning: When planning for retirement, don’t just consider your current expenses. Project how inflation might affect your future purchasing power. The Social Security COLA 2026 is a reminder that costs continue to rise. Incorporate realistic inflation assumptions into your retirement budget to ensure your savings and investments can keep pace.

6. Consulting a Financial Advisor: Social Security claiming strategies can be complex, especially when considering individual circumstances, spousal benefits, and other retirement income sources. A qualified financial advisor specializing in retirement planning can provide personalized guidance to help you make the most informed decisions.

The Long-Term Outlook for Social Security

While the Social Security COLA 2026 provides a short-term adjustment to benefits, it’s also important to consider the long-term solvency of the Social Security program. The Social Security trust funds are projected to be able to pay 100% of promised benefits until the mid-2030s. After that, without congressional action, benefits would reduce to approximately 80% of scheduled amounts. This long-term outlook is a subject of ongoing debate and legislative proposals.

Potential solutions to ensure the long-term solvency of Social Security include raising the full retirement age, increasing the Social Security tax rate, adjusting the wage base subject to Social Security taxes, changing the COLA calculation method (e.g., switching to the Chained CPI), or a combination of these and other measures. While these discussions are complex and politically sensitive, they are crucial for the future of the program.

For current and future beneficiaries, understanding these long-term challenges is important for holistic retirement planning. While the Social Security COLA 2026 ensures your benefits keep pace with inflation in the near term, having diversified retirement income sources—such as personal savings, 401(k)s, IRAs, and other investments—provides a stronger financial foundation, regardless of potential future adjustments to the Social Security system.

Preparing for the 2026 Social Security COLA

As the projected 3.2% Social Security COLA 2026 approaches, there are several steps you can take to prepare:

1. Review Your Budget: With an anticipated increase in benefits, take the opportunity to review your current budget. See how the additional income might affect your spending or savings plans. Even a modest increase can provide more flexibility in covering essential expenses or allocating funds to other financial goals.

2. Check Your "My Social Security" Account: This online portal is an invaluable resource. You can view your earnings record, get personalized benefit estimates, and stay updated on important announcements from the SSA. Ensure your contact information is current so you receive all relevant communications.

3. Stay Informed: Keep an eye on official announcements from the Social Security Administration, typically made in October of the year prior to the COLA taking effect. While the 3.2% Social Security COLA 2026 is a strong projection, the final figure will be confirmed then. Stay informed about any legislative discussions regarding Social Security reform that could impact future benefits.

4. Re-evaluate Your Retirement Plan: The COLA is a consistent reminder that retirement planning is an ongoing process. Use this opportunity to re-evaluate your overall retirement strategy. Are your savings on track? Are your investments performing as expected? How do your anticipated Social Security benefits fit into your broader financial picture?

5. Consider Professional Advice: For complex financial situations or if you have specific questions about how the Social Security COLA 2026 impacts your unique circumstances, consider consulting a financial advisor or a Social Security specialist. They can offer tailored advice and help you optimize your benefits.

The Social Security COLA 2026, projected at 3.2%, represents a continued effort to protect the purchasing power of millions of Americans. By understanding how this adjustment works, its relationship with inflation, and its potential impact on your personal finances, you can make informed decisions to secure your financial future. Proactive planning, staying informed, and leveraging available resources are key to navigating the evolving landscape of Social Security benefits and ensuring a stable and comfortable retirement.

Conclusion: Embracing the Social Security COLA 2026 for a Secure Future

The projected 3.2% Social Security COLA 2026 is more than just an annual adjustment; it’s a vital mechanism designed to safeguard the financial well-being of millions of Americans against the relentless erosion of inflation. For retirees, individuals with disabilities, and survivors, this increase represents a tangible commitment to maintaining their standard of living, allowing their benefits to keep pace with the rising costs of everyday necessities. While the exact figure will be confirmed later, the current projection provides a valuable benchmark for individuals to begin their financial planning for the upcoming year.

Understanding the intricacies of the COLA calculation, its historical context, and its interaction with other financial factors like Medicare premiums and taxes is paramount. It empowers beneficiaries to look beyond the headline number and grasp the deeper implications for their personal finances. The 3.2% Social Security COLA 2026 serves as a powerful reminder that continuous financial vigilance and strategic planning are not merely options but necessities in today’s dynamic economic environment.

Furthermore, this adjustment underscores the importance of a holistic approach to retirement. While Social Security provides a foundational income, it is often most effective when complemented by diversified savings, investments, and well-thought-out claiming strategies. Delaying benefits, coordinating with a spouse, and ensuring your earnings record is accurate are all proactive steps that can amplify the impact of any COLA, including the Social Security COLA 2026, on your overall financial security.

As we move towards 2026, staying informed through official Social Security Administration channels, regularly reviewing your financial situation, and seeking expert advice when needed will be crucial. The Social Security COLA 2026 is a positive step in ensuring that your hard-earned benefits retain their value, contributing to a more secure and predictable financial future. Embrace this adjustment as an opportunity to reinforce your financial planning and continue building a resilient foundation for your retirement years.

Contributions Now")

in 2025: Boost Contributions by 10% Annually")